Income Tax Slabs 2026-27 — New vs Old Regime Comparison

Table of Contents

New Tax Regime -- FY 2026-27 (AY 2027-28)

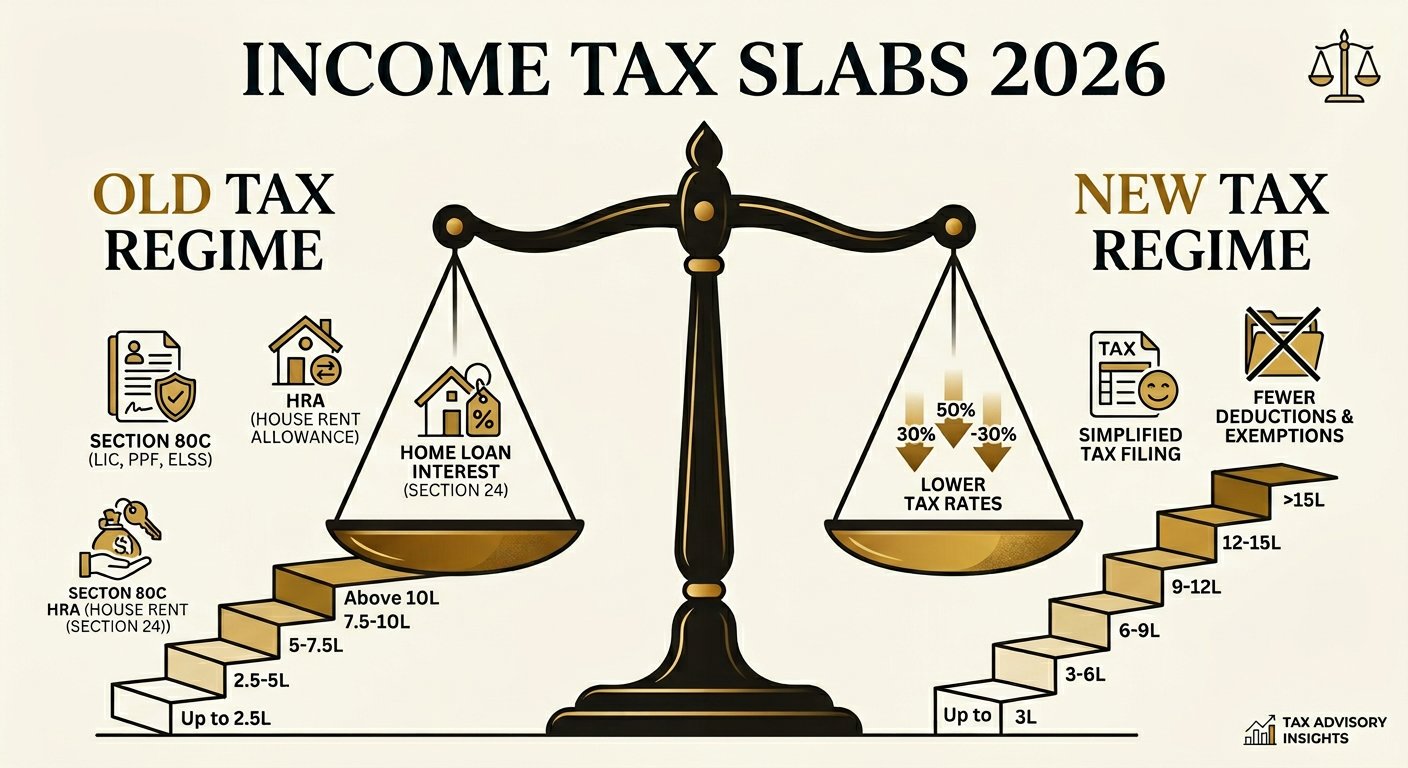

Every February, my Karol Bagh office fills with salaried employees asking which regime to choose. After analyzing 1,000+ returns, the answer depends on your deductions. The new tax regime (Section 115BAC) has been the default regime since FY 2023-24. It offers lower tax rates but fewer deductions and exemptions.

| Income Slab (₹) | Tax Rate |

|---|---|

| 0 - 4,00,000 | Nil |

| 4,00,001 - 8,00,000 | 5% |

| 8,00,001 - 12,00,000 | 10% |

| 12,00,001 - 16,00,000 | 15% |

| 16,00,001 - 20,00,000 | 20% |

| 20,00,001 - 24,00,000 | 25% |

| Above 24,00,000 | 30% |

- Standard deduction: ₹75,000 (salaried & pensioners)

- Rebate u/s 87A: Up to ₹60,000 (effective tax-free income up to ₹12 lakh for salaried)

- Surcharge: 10% above ₹50L, 15% above ₹1Cr, 25% above ₹2Cr

- Cess: 4% Health & Education Cess on tax + surcharge

• Gross income: ₹12,00,000

• Standard deduction: ₹75,000

• Taxable income: ₹11,25,000

• Tax: ₹4,00,001-8,00,000 @5% = ₹20,000 + ₹8,00,001-11,25,000 @10% = ₹32,500

• Total tax: ₹52,500

• After 87A rebate (₹52,500): ₹0

• Net tax = ZERO

Old Tax Regime -- FY 2026-27

The old regime allows all traditional deductions and exemptions. It benefits taxpayers who have significant investments under Section 80C, home loan interest, HRA, and other deductions. In my experience, if your total deductions exceed ₹3.75 lakh, the old regime saves you money.

| Income Slab (₹) | Tax Rate |

|---|---|

| 0 - 2,50,000 | Nil |

| 2,50,001 - 5,00,000 | 5% |

| 5,00,001 - 10,00,000 | 20% |

| Above 10,00,000 | 30% |

- Section 80C: Up to ₹1.5 lakh (PPF, ELSS, LIC, NPS, home loan principal)

- Section 80D: Up to ₹25,000 (₹50,000 for senior citizens) medical insurance

- HRA exemption: For salaried staying in rented accommodation

- Section 24(b): Up to ₹2 lakh home loan interest

- Standard deduction: ₹50,000

Side-by-Side Comparison

| Feature | New Regime | Old Regime |

|---|---|---|

| Basic exemption | ₹4,00,000 | ₹2,50,000 |

| Standard deduction | ₹75,000 | ₹50,000 |

| Section 80C | Not available | Up to ₹1.5L |

| HRA exemption | Not available | Available |

| Home loan interest | Not available | Up to ₹2L u/s 24(b) |

| Rebate 87A | Up to ₹60,000 | Up to ₹12,500 |

| Default regime | Yes | Must opt-in |

Tax Calculation Examples

Let me show you with real numbers -- these are the kinds of calculations I do every day for clients in my Delhi office:

Example 1: Salaried, ₹10 lakh income, minimal deductions

| New Regime | Old Regime | |

|---|---|---|

| Gross income | ₹10,00,000 | ₹10,00,000 |

| Standard deduction | ₹75,000 | ₹50,000 |

| Sec 80C | -- | ₹1,00,000 |

| Taxable income | ₹9,25,000 | ₹8,50,000 |

| Tax | ₹40,000 | ₹72,500 |

| After rebate | ₹0 | ₹60,000 |

Winner: New Regime -- saves ₹60,000 thanks to the 87A rebate.

Old Regime: Taxable = ₹18L - ₹50K - ₹5.55L = ₹11.95L → Tax = ₹1,73,500 + 4% cess = ₹1,80,440

New Regime: Taxable = ₹18L - ₹75K = ₹17.25L → Tax = ₹2,13,750 + 4% cess = ₹2,22,300

Old Regime saves ₹41,860!

How to Choose the Right Regime

- Choose New Regime if: Income below ₹12L (salaried), minimal investments, want simplicity

- Choose Old Regime if: You claim ₹3.75L+ in deductions, have home loan, significant 80C investments

- Use our Income Tax Calculator to compare both regimes with your actual income and deductions